Students deciding this week whether to attend graduate school in the fall are navigating the end of a 20-year era of student loan policy. More students will need to find private loans, making access to credit an important factor in determining who can afford graduate programs.

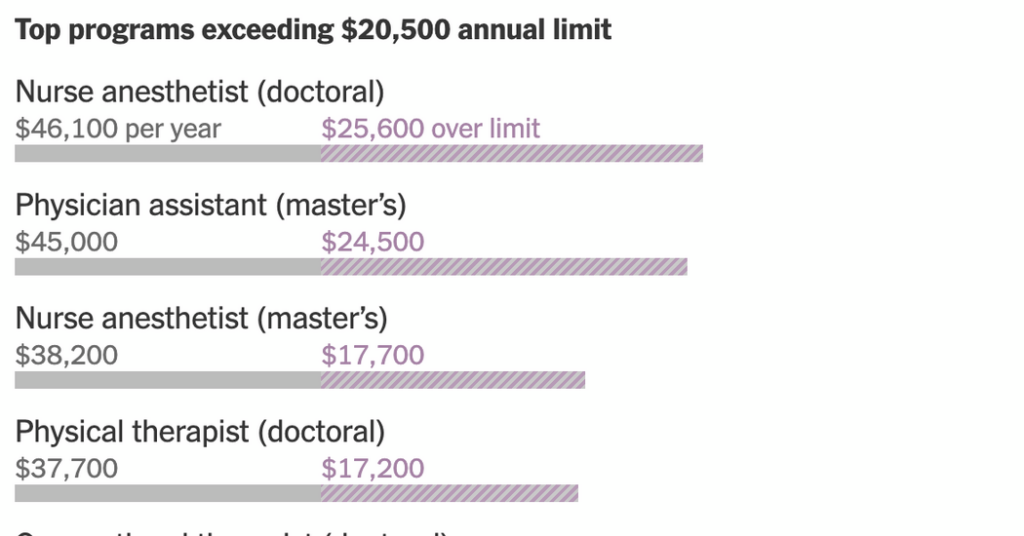

Take the master’s degree for physician assistants: On average, borrowers take out $45,000 per year for a two-year program. Students were once able to borrow up to the entire cost of tuition and expenses from the U.S. government, but the major policy bill signed by President Trump last year capped federal student loans for most graduate schools at $20,500 a year.

At many expensive programs, especially in health-related fields, that is often not enough to cover the cost.

That means aspiring physician assistants may have to find an average of $24,500 in private loans starting this summer, and some may not be able to secure those loans at all.

An analysis of borrowing and credit history data from 2015 to 2024 by the Philadelphia Federal Reserve found that 28 percent of graduate students taking out loans would exceed today’s new limits, and about four in 10 of them would have trouble getting supplemental private loans without a co-signer.

“The end effect is to essentially make it so that graduate school is only accessible to students from the wealthiest families,” said Jennifer Zhang, an analyst at Protect Borrowers, an advocacy group that issued a report last month looking at private lending standards.

A few graduate programs in fields like law, medicine and dentistry have higher federal borrowing limits at $50,000 a year. Even then, the limits aren’t enough in many cases.

Jordan Matsudaira, an author of the Philadelphia Fed report and now a professor at American University, said that since a lot of students are going to hit the federal limits, the issue “is really about how many of them are going to have a hard time finding alternative sources of financing in the private market.”

These average loan amounts come from a report that Professor Matsudaira helped produce while he was chief economist at the Education Department. The report was taken down from the department’s website shortly after Mr. Trump took office. While other government sites include information on borrowing, the report, which covers loans between 2020 and 2023, remains the most detailed and recent snapshot of annual borrowing.

The data provides a useful look into how much it costs to attend over 100 graduate programs across the country, college by college — and which of them may have more students who will need to find private loans.

At the vast majority of dental programs, for example, the average borrower took out far more than the $50,000 yearly limit. (Just seven dental schools in the data had an average annual loan under that amount.)

You can look up individual programs and colleges at the bottom of this article.

Many programs will be unaffected: There are many degrees where a majority of colleges have average loans that are well under the cap, so most students could still borrow the entire cost from the federal government.

For instance, most M.B.A. programs in the data have average annual loan amounts below the $20,500 federal limit. Even then, quite a few still fall above that cutoff.

Previously, the federal government made financing graduate education straightforward: Borrowers could take out as much money as they needed at a known interest rate. But with the new caps, more students will need to turn to private lenders. Some borrowers may face higher interest rates, and those with lower credit, lower incomes or who lack a co-signer may have trouble getting loans at all.

“Lenders can’t lend blindly,” said Scott Buchanan, executive director of the Student Loan Servicing Alliance, a nonprofit trade association that represents student loan service providers.

The borrowing caps come alongside other changes in federal student loan policy that make financing graduate education more challenging. Those include ending a more generous loan repayment program, adding restrictions on qualifying for federal student loan forgiveness, and no longer lending to programs whose graduates fail to meet certain income requirements.

“Those coming together at the same time is really kind of a recipe for disaster,” said Aissa Canchola Bañez, policy director at Protect Borrowers. She said she was worried that more vulnerable students could be pushed into subprime loans with higher interest rates if they couldn’t get loans from traditional lenders.

Senator Elizabeth Warren, Democrat of Massachusetts, said in a statement that the loan caps would “force even more families to turn to the predatory private loan market to afford their ticket to the American Dream.” Earlier this year, she and eight other senators released the findings of an investigation into private lenders. It found that many of them had failed to offer all the protections of federal loans, and some had sold student loans to private equity firms.

How we got here

The bill signed into law last July eliminated the Grad PLUS loan program for all students starting graduate school after July 1, 2026. The program let graduate students borrow up to the total cost of attendance, a figure calculated by each school that includes tuition, fees, health insurance and living costs. Grad PLUS loans required a basic credit screening for loan approval but did not take credit scores into account. Once approved, all borrowers received their loans at the same rate, currently set at just under 9 percent.

Graduate school was already becoming a more popular option when the loan program was created in 2006. Since then, the number of students going to graduate school and the amount they have borrowed have continued to grow. The average amount that graduate borrowers have been taking out for their degrees roughly doubled from $35,000 in 2004 to $69,000 in 2020, rising faster than inflation. Over the same period, the number of graduate degrees awarded each year increased by over 340,000, nearly 50 percent more.

Preston Cooper, a senior fellow at the American Enterprise Institute, supports the loan caps and says Grad PLUS “encouraged schools to let cost inflation get out of control because schools could be confident that they could raise tuition for graduate programs and pass the cost along to students.”

A study of programs in Texas found that after the introduction of Grad PLUS loans, loan amounts increased, with the majority of the additional money borrowed going toward tuition increases.

Other reviews of programs like law, business and medicine found that while tuition did go up after Grad PLUS, the increases kept pace with inflation.

Requesting to be labeled ‘professional’

Private loan companies vary their interest rates but typically offer rates between 3 and 15 percent, though some can be higher. Traditionally, credit history has determined who gets a loan and at what rate, but in response to the expected increase in demand for private loans, the industry has been exploring alternatives like income sharing agreements, or lending methods that look at future earnings potential.

Many programs, including social work, aviation and nursing, have been asking the Education Department to be labeled “professional” so they can be eligible for the $50,000 loan caps. Currently, the department has decided on a list of 11 programs it has classified as “professional” and thus eligible for the higher limits.

In the meantime, colleges are preparing for the new caps. Midwestern University is a private nonprofit university with two campuses in Arizona and Illinois. It offers graduate programs in health science fields, including dentistry, osteopathic medicine and physical therapy, many of which are expected to go over the loan limits. The college is looking to expand scholarship offerings, financial aid and its own internal loan program.

“We clearly are anxious to see what the changes in the federal caps will bring,” said Gregory O’Coyne, the university’s vice president for finance.

Amy Fan is a Times reporter and a member of the 2025-26 Times Fellowship class, a program for journalists early in their careers.

The post Getting a Loan for Grad School Is About to Get More Complicated appeared first on New York Times.