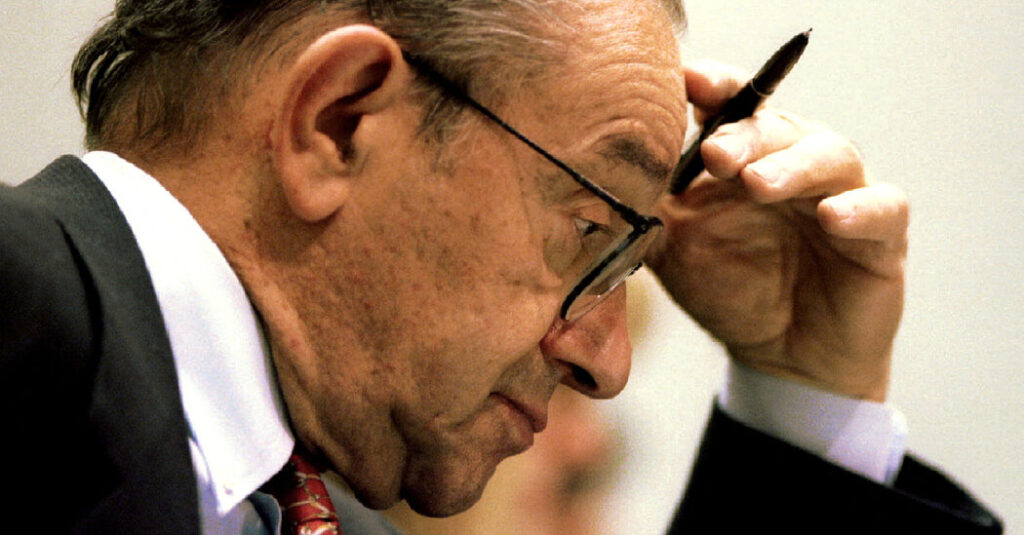

Whatever else, Alan Greenspan should be remembered for what is surely the rarest virtue among public officials: admitting error.

The moment was Oct. 23, 2008. The American financial system was in tatters. Bear Stearns and Lehman Brothers were bust, and the government had taken equity stakes in private banks in a bid to arrest the crisis. Americans were swamped with mortgage debt and suffering through a brutal recession.

Mr. Greenspan, the former chairman of the Federal Reserve, had retired less than three years earlier. No one had championed the free market system or worked to block financial regulation, which he disparaged as both harmful and unnecessary, with more ardor than he had. As head of the most powerful of the agencies that regulated banks, he hadn’t used his authorities to quash the bubble in mortgage lending.

Mr. Greenspan was no corporate toady or business apologist. He was an honest and inquisitive intellectual committed to the principles of Adam Smith, principles that work well most of the time.

This was not one of those times, and his conviction was shaken. “Those of us who have looked to the self-interest of lending institutions to protect shareholders’ equity, myself included, are in a state of shocked disbelief,” he confessed that day to the House Committee on Oversight and Government Reform.

Mr. Greenspan questioned the principles he had developed as a young disciple of Ayn Rand and employed in a storied career as an adviser to corporate chieftains and later to U.S. presidents.

“The modern risk-management paradigm held sway for decades,” he said, referring to the esoteric economic models that had assured traders of the soundness of the billions in securities that had been layered on top of home mortgages — securities that in 2007 and 2008 suffered tremendous losses and caused banks to fall like dominoes. “The whole intellectual edifice, however, collapsed in the summer of last year.”

Under grilling from Representative Henry Waxman, the committee chairman, Mr. Greenspan bluntly admitted he had made “a mistake.” Although he tried to blame it on a “flaw” in the models, his admission was striking for one who had flown very high — a comedown that should be imprinted in the memory of every person in a position of responsibility over economic policy.

Alan Greenspan was the country’s first and possibly last celebrity Fed chairman. He moved in a world of diplomats and stars — his second wife was the journalist Andrea Mitchell — and for nearly 20 years, his words moved markets. Stockbrokers as well as ordinary people parsed them for clues to the future, though it sometimes took a lexicographer to decipher his convoluted phrasing. A friend used to call me when some pronouncement of the chairman’s was creating havoc in the stock market: “What is he saying?” he would excitedly demand. “What is he saying?!” (Kevin Warsh, confirmed as the Fed chair last month, seems to have adopted Mr. Greenspan’s penchant for abstruse language.)

Mr. Greenspan guided the Fed’s Board of Governors with a polished and seemingly effortless touch. In Congress, he claimed respect from both parties — quite a feat given his right-wing philosophy. Nominated for a fifth term in 2004, he was confirmed by the Senate with just one dissenting vote. More recent Fed chiefs got more than a dozen. In 1999, Phil Gramm, chairman of the Senate Banking Committee, told Mr. Greenspan, “You will go down as the greatest chairman in the history of the Federal Reserve Bank.”

Even if Fed chairs tend to be given too much credit or blame for events on their watch, Mr. Greenspan presided over what was then the longest peacetime economic expansion in U.S. history, lasting from 1991 to 2001.

But even during that prosperous decade, the themes of his response to the later mortgage bubble were present.

As Mr. Greenspan described in his memoir, his approach solidified in the mid-1990s, a time when the stock market was soaring and new cable news programs and their small-investor fans were suddenly taking an interest. In November 1995, the Dow Jones average cracked 5,000, a milestone that represented a doubling in only five years; by the following October the Dow was at 6,000. Shortly after, Mr. Greenspan addressed the annual dinner of the American Enterprise Institute in Washington; he wondered aloud whether stocks were showing signs of “irrational exuberance.” The next morning panicky traders, fearing that the Fed would intervene, rushed to sell, and the Dow plunged nearly 150 points, although it immediately recovered.

As stocks continued their breathtaking rise, Mr. Greenspan confided in his fellow governors that they might have to raise interest rates to quash speculation. By the following spring, the Dow neared 7,000. The Fed raised rates, and the market fell. But once again, it came roaring back. By June, the Dow was at 7,800.

Humbled, Mr. Greenspan concluded, “You can’t tell when a market is overvalued, and you can’t fight market forces.” He never tried to rein in stock prices again.

And so, a pattern: Ignore bubbles as they inflate, intervene if and as necessary to clean up the mess after they pop. In 1998, after the sudden collapse of a giant hedge fund, he led the Fed to cut interest rates three times to stabilize markets. Within weeks of those cuts, eBay went public, and its shares tripled on the opening day of trading. Greased by cheap money, dot-com stocks inflated in a new bubble. After they collapsed, and after a spate of corporate scandals, Mr. Greenspan rushed to the rescue again, cutting the overnight Federal Funds rate until it reached 1 percent. Mr. Greenspan’s light touch was enough to contain these emergencies — but not the larger one to come.

Raised by a single mom during the Great Depression, Mr. Greenspan, who played saxophone for a jazz band before becoming a big-time consultant and obtaining a doctorate in economics, was the first Fed chief to think broadly about the revolution in computer technology, and it seduced him. Again and again, he expressed the belief that computers would increase productivity and thus allow the Fed to cut rates further than previously thought possible without stoking inflation. He was prescient in seeing the computer’s power, and his resistance to intervening in bubbles would have been correct had he applied it with a little discretion.

By the end of his time at the Fed, a huge bubble was inflating. Mortgage brokers were peddling loans without requiring borrowers to document their earnings, a sign of troubling excess in the most important asset for ordinary Americans: their homes.

The central bankers’ cliché that one never “knows” a bubble for sure was true, but the Fed’s job is to weigh relative risks, not certainties. Signs of froth in mortgages were omnipresent; buyers were getting full financing at teaser interest rates; speculators chasing quick flips were posing as buyers; 40 percent of mortgages were going to subprime buyers and those who lacked documentation.

Mr. Greenspan made much of the “blunt tool” argument — that raising interest rates risked penalizing the entire economy merely to cool the housing sector. This betrayed the Fed’s metamorphosis into an institution of elites: government and academic economists who live in a world of computer models. Before the Greenspan era, the Fed was closer to its original design, an institution of bankers entrusted with safeguarding the banking system.

The Fed and its sister regulators had specific tools to stem the crisis — at a minimum, they could have demanded that mortgage banks obtain proof of their clients’ income and give loans only to people who could repay them. Mr. Greenspan, the celebrity Ph.D., focused on the highbrow work of determining interest rates; he failed to crack down on hyper-permissive lending terms — grubby, detailed work in which Mr. Greenspan never showed any interest.

In recent times, Fed governors with real-world lending experience have become so rare that their absence is not even noticed. Mr. Greenspan shaped how modern central banks operate. But even he had to admit that his infatuation with models had been wrong. The country’s financial leaders might remember that humbling moment in 2008 and what it showed: Overconfidence and complacency can mar even the most storied of reputations.

Roger Lowenstein is a journalist and the author of “America’s Bank: The Epic Struggle to Create the Federal Reserve,” “Buffett: The Making of an American Capitalist” and “Ways and Means: Lincoln and His Cabinet and the Financing of the Civil War.”

The Times is committed to publishing a diversity of letters to the editor. We’d like to hear what you think about this or any of our articles. Here are some tips. And here’s our email: [email protected].

Follow the New York Times Opinion section on Facebook, Instagram, TikTok, Bluesky, WhatsApp and Threads.

The post Alan Greenspan Was Wrong About One Thing. It Was a Big One. appeared first on New York Times.