A law that went into effect in 2024 was supposed to help persuade more people to save for college.

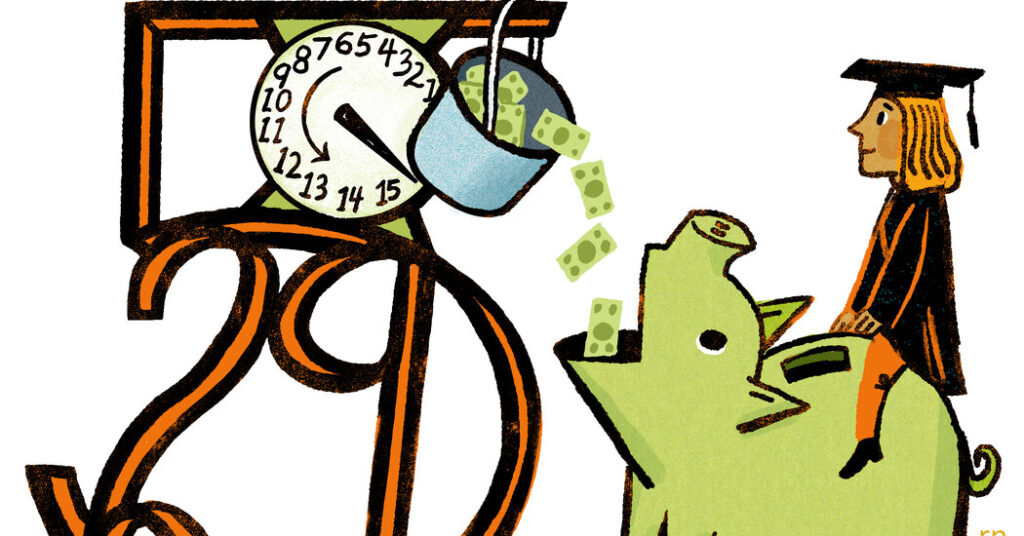

As of Jan. 1 that year, you could begin moving up to $35,000 from a 529 college savings account into a Roth individual retirement account, as long as you followed a long list of rules. Some of those rules outlined eligibility, and the legislation that allowed for the transfer refers to “a qualified tuition program of a designated beneficiary” that has been maintained for 15 years.

But does the beneficiary need to stay the same for 15 years, or does the account simply need to have been open for that long? The language isn’t completely clear.

Plenty of people need clarity here, since lots of families change the beneficiaries on 529 accounts for any number of reasons. So if you’re a parent who opened an account in your own name and didn’t change the beneficiary to your child until that child was 17 years old, did you inadvertently reset that 15-year clock, causing any rollover to be impossible until the child is 32?

The answer has six-figure implications. After all, if you put $35,000 in a Roth account for a 27-year-old and it earns 7 percent annually over 40 years, the balance will grow to more than $524,000. If the money has just 30 years to compound because the 15-year rule led to a later start for the Roth, you end up with $266,000.

When you open a 529 account, there is one account owner and one beneficiary. You can open an account for yourself to pay for your own educational expenses, in which case you are the owner and the beneficiary. But usually, the account owner — say a parent or a grandparent — has a child’s future education in mind.

There are many possible reasons, however, for not naming that child as a beneficiary right away. Maybe you’ve rushed to open the account after the positive pregnancy test, and then you forget to update the beneficiary with the baby’s name later on. Or maybe you’re a grandparent who finds it easier to have just one account, with some vague plan to swap beneficiaries in and out later once you see how many grandchildren you have.

At Ascensus, which claims about half of the 529 administration market for accounts where owners make investments directly, any change in account beneficiary requires what is technically a new account. But now, an increasing number of knowledgeable 529 account owners are worried that a beneficiary change — and that new account — can reset that 15-year clock.

The College Savings Plan Network, which represents state government officials and others in the 529 industry, saw the confusion coming not long after the legislation, the SECURE 2.0 Act, passed. In September 2023, it sent a letter to the Treasury Department asking for official clarification and making its case for not resetting the 15-year clock because of a beneficiary change.

The organization made a good point: Congress was trying to build more flexibility into 529 plans by allowing the rollover, even as it created the 15-year rule to make sure people weren’t opening 529 accounts late in the teenage years intending them to really be Roths and not for education.

“Requiring a reset of the 15-year rule each time an account owner, designated beneficiary or administrative change is made to an account would contravene congressional intent,” the letter said.

Nearly three years later, however, there has been no answer from the Treasury Department. A 2025 document outlining the department’s priorities does suggest that guidance could come as soon as next month.

Michael L. Hadley, a benefits lawyer in Washington, said the Internal Revenue Service had made it clear that its priority was establishing regulations for carrying out the One Big Beautiful Bill Act.

“The 529 issue is on their project list, but it’s really just a resources issue, I think,” he said.

It would be surprising if the Treasury Department declared that any change in beneficiary restarted the 15-year clock. Then again, strange things happen in Washington these days.

The best way to protect yourself is to maintain good beneficiary hygiene. If you think you might have money left over from your 529 — because a child doesn’t go to college or gets a big scholarship or goes to West Point for free — and you want to use those funds for a Roth, then make that child the beneficiary as early as possible. And if you have more than one child, have an account for each.

If the 529 industry gets what it wants, any beneficiary change will not have mattered for Roth rollover purposes. And if it doesn’t, you’ll probably be glad you made the change.

Ron Lieber has been the Your Money columnist since 2008. His beat is beating the system.

The post Want to Move 529 Account Money to a Roth I.R.A.? There’s a Hitch. appeared first on New York Times.