The Iran war is stoking investor fears of a widening conflict, a 1974-like energy crisis, a global recession and the demise of this bull market. But between all the fires and explosions, it will pay to keep a cool head.

War’s human cost is horrid. But capital markets are cold-hearted. Regional conflicts – however tragic – never faze stocks or oil prices for long.

Their trajectory follows a simple, three-step pattern: 1) Volatility and oil prices surge ahead of the conflict as saber-rattling raises uncertainty, 2) Initial fighting further gooses volatility and prices as markets digest worst-case scenarios, then 3) Stocks begin to rally – well before the fighting stops – as investors fathom the conflict’s limited and temporary economic footprint, realizing that global growth isn’t stopping, after all.

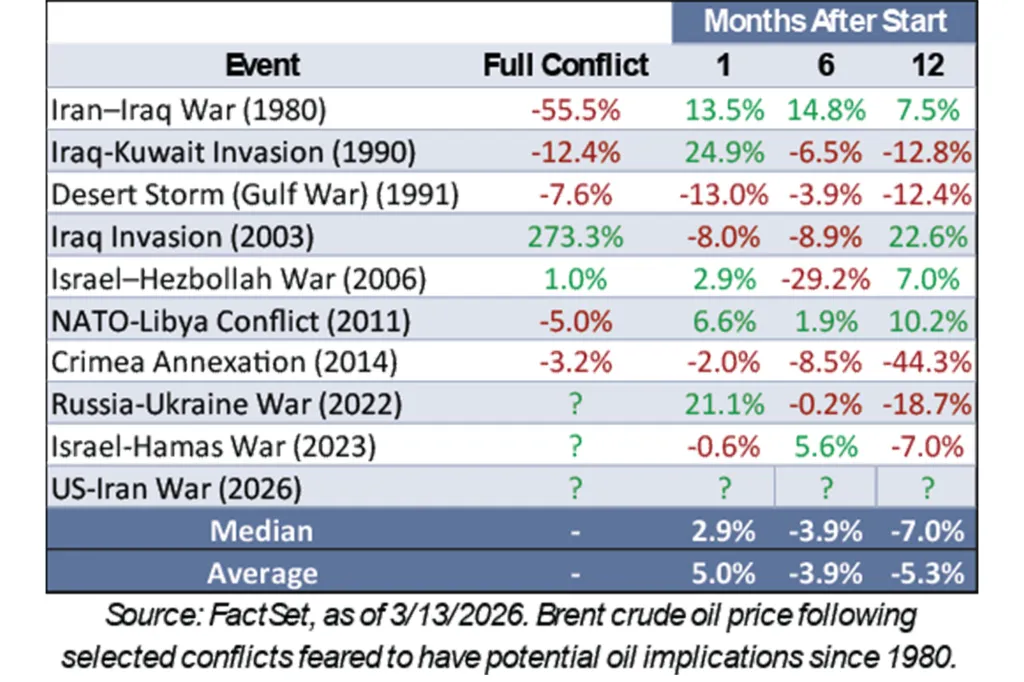

The S&P 500 jumped 12.5% during Desert Storm and 31.9% in the 12 months after its outbreak. Afghanistan’s and Iraq’s “forever wars” showcased long, multi-front fighting that failed to thwart bull markets. The run-up to 2003’s Iraq invasion evolved at the end of the long 2000-2003 bear market. World and US stocks rocketed 33.1% and 28.7%, respectively, in 2003 as bombs didn’t blast stocks or GDP.

They won’t this time, either.

Yes, Russia’s Ukraine invasion happened early in a small, short bear market. It also involved energy. But coincidence isn’t causation. Other myriad forces stung investors in 2022’s rare, sentiment-induced recession-less bear market – inflation, supply chain chaos, Fed hikes, yield curve inversion and more amid frothy sentiment and elevated stock supply entering 2022. Besides, stocks bottomed that fall while fighting, sadly, continues now.

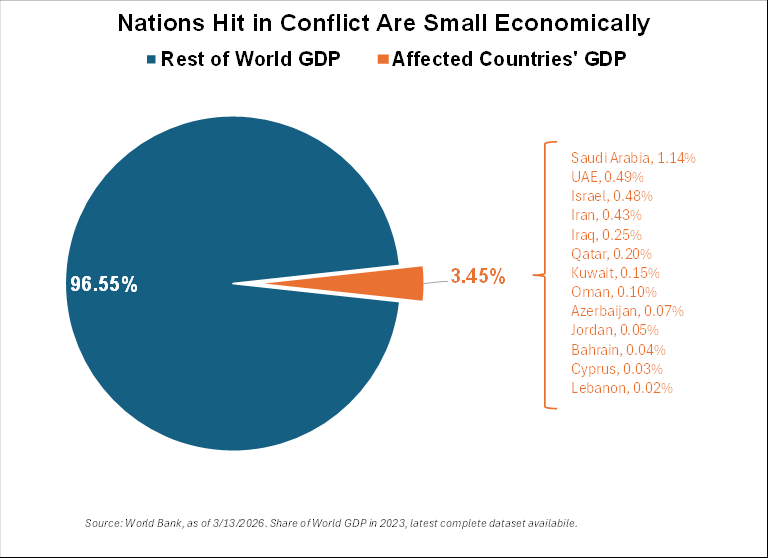

The Gulf Coast’s role as a production hub and transit chokepoint sparks widespread fear. Yet these countries generate just 3.5% of global GDP. Iran supplied just 3% of global oil output pre-war. Analysts previously estimated a 2026 3% global oversupply. Iran’s oil exports go primarily to China – which increased purchases 16% in January and February, seemingly stockpiling for this.

The key? Shipping. Legendarily, 20% of global oil flows through the now closed Strait of Hormuz. But almost a third of that is entering for processing, not exiting. That now goes elsewhere. And pipeline workarounds for almost a third of Hormuz-impacted oil already exist.

This isn’t the 1970s. Then, America was an energy weakling. Most of the Middle East hated us. Now America is the world’s top producer – an exporter with strong relationships with most all the region’s exporters except Iran. In the ‘70s it took almost a barrel of oil to generate $1,000 in inflation-adjusted US GDP. Now? A quarter of that.

Markets will soon grasp all this, pre-pricing the Strait’s reopening, even if fear-based investors can’t. Oil likely falls back to January’s pre-war levels. Consider: In the nine major oil-tied regional wars since 1980, oil prices averaged 5% higher a month after the conflict’s start – but 4% lower than at its start after six months and 5% lower a year out.

Oil rose from $55 to $67 before the Iran bombings. Expect the low end of that range as conflict ends.

If I’m wrong? Oil was over $75 a barrel for almost all of 2023. Global GDP was fine and global stocks rose over 22%. In the early 2010s, economies and stocks grew for years with $100 oil. With about 45% inflation since then, $100 oil now is equal to $65 oil then.

Politically, if this conflict is unresolved by August, Republicans will suffer hugely in midterms. That likely happens somewhat anyway, though, as my 2026 forecast showed – but is also “yuge” motivation for Trump to end this saga swiftly.

So don’t panic. Stocks will soon consider this war with cool detachment. You should, too.

Ken Fisher is the founder and executive chairman of Fisher Investments, a four-time New York Times bestselling author, and regular columnist in 21 countries globally.

The post How investors should think about oil and stocks in the Iran war – in 3 simple steps appeared first on New York Post.