Google the price of oil, and you’ll most likely find two widely quoted prices for the commodity, one in the United States, the other in Europe.

These prices, which change many times a minute on electronic markets, suggest that although the war with Iran has made energy a lot more expensive, things are not nearly as bad as they were four years ago, after Russia invaded Ukraine.

But if you needed an actual tanker full of oil — and quickly — it would cost you dearly.

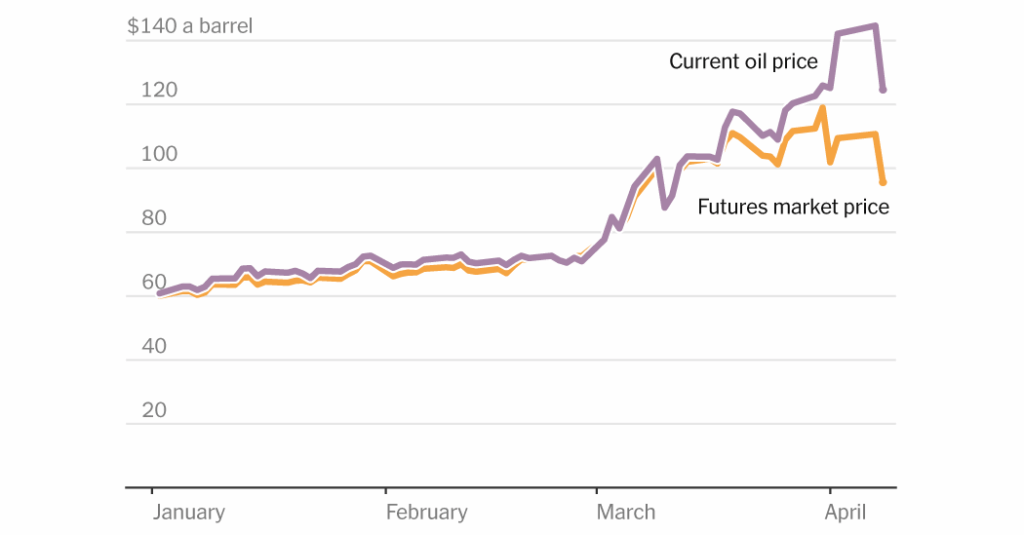

On Tuesday, before President Trump said the United States and Iran had reached a cease-fire agreement, a commonly cited price of Brent oil, the European one, was about $109 a barrel. That was well below highs reached in 2022, when that price briefly topped $130, without adjusting for inflation.

But in the market where energy companies buy and sell liquid oil transported on ships, the price was almost $145 a barrel, a record and more than double the price before the United States and Israel attacked Iran on Feb. 28, according to Argus Media, a company that tracks commodity prices.

The reason the two prices were so different is that the first, more commonly cited price is the futures price. It reflects how valuable traders think oil will be in a month or two and functions a lot like the stock markets. The second is often called the spot price, and it is tied to the delivery of many tons of crude oil, which a refinery can turn into gasoline, diesel and jet fuel.

The futures and spot prices are rarely exactly the same, but the gap between them has grown unusually big in the past few weeks, so much so that oil executives and analysts say futures prices no longer accurately reflect the extent of the supply shock that the world is experiencing.

“The futures market is not representing the on-the-ground and on-the-water reality of oil at all,” said Vikas Dwivedi, global energy strategist at Macquarie Group, an Australian financial services firm. “It’s quite broken.”

Mike Wirth, the chief executive of Chevron, the second-largest U.S. oil company, expressed similar concerns last month at a Houston energy conference, CERAWeek by S&P Global.

“Physical prices and physical supplies would reflect a tighter market than I think the forward curve reflects,” Mr. Wirth said, referring to the futures market.

Spot and futures prices often diverge during big market disruptions, such as the Covid-19 pandemic and Russia’s invasion of Ukraine. International upheavals magnify the difference between the value of oil today and two months from now.

But the spread between the two prices in recent days dwarfs that of any other period in the past 20 years, Argus data show. Even energy analysts have struggled to explain why that gap is so large this time.

“It is a mystery,” Mr. Dwivedi said.

What is clear is that the war with Iran has upended oil markets in profound ways. Estimates indicate that companies have turned off 10 percent or more of the world’s oil supply since the war started because they cannot safely get tankers through the Strait of Hormuz, the narrow waterway between Iran and the Arabian Peninsula.

Prices have soared around the world. And some countries in Asia — which depends heavily on fuel from the Persian Gulf — have even faced shortages. Gas stations in Vietnam and Thailand turned away customers, saying they had no fuel; Sri Lanka declared every Wednesday a public holiday; and many other countries have mandated or encouraged remote work.

The two-week cease-fire with Iran sent oil prices plunging in the hours after Mr. Trump announced the deal, but very little has changed on the ground. Shipping companies remain wary of sending vessels through the strait. That means that a substantial portion of the world’s oil is still trapped in the Persian Gulf.

“The physical price just tells you how tight everything is right now,” said Jason Gabelman, an energy analyst at the investment bank TD Cowen.

Rebecca F. Elliott covers energy for The Times.

The post The Oil Shock Is Worse Than You Think appeared first on New York Times.