For much of the war in Iran, investors have clung to a rosy outlook. As long as the conflict ended quickly, economic optimism underpinned by a growing economy and healthy corporate profits could still return.

That’s starting to change.

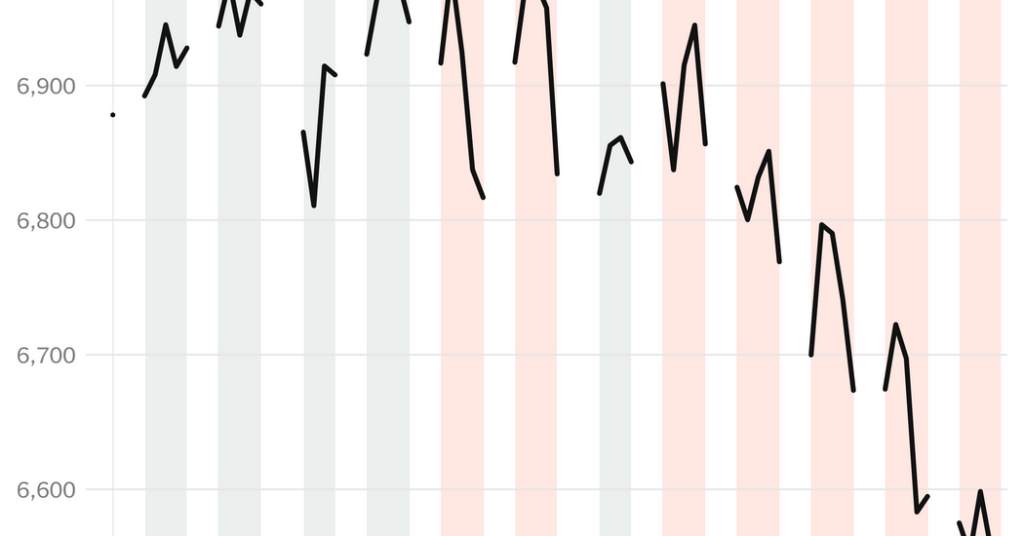

With another drop on Friday, the S&P 500 notched its worst week of losses since the war began, its fifth straight week of losses and its worst weekly losing streak in roughly four years. It is now set to record its worst monthly performance since March 2025, when inflation worries preceded the sharp tariff-induced sell-off in April.

But this month’s drop is only around half of that prompted by the tariff proposals, and it has taken much longer to get there. After four weeks of war, the S&P 500 is close to 9 percent below its last record high, in January.

To some investors, this is a relatively modest decline given the economic threat posed by the war. Since the fighting began last month, oil prices have risen to roughly twice the price they were at the start of the year, fueling fears of inflation as companies and consumers pay more for energy products

But the trading also reflects the market’s dependence on an administration known for quickly changing course. The situation could get a lot worse in Iran, but also could quickly get a lot better, and many investors feel they need to be prepared for both scenarios.

“We still have this underlying theme in the market that if investors take a thought or fear too far, they are going to miss out on the recovery when the market goes higher,” said Cindy Beaulieu, chief investment officer for North America at the investment manager Conning. “It is still a FOMO market.”

President Trump’s sensitivity to the market was on display again Thursday, when after a further slide in stocks and sharp rise in oil prices, he extended the deadline for Iran to either open the Strait of Hormuz, a vital oil shipping passage, or face strikes on its power plants.. Hours later, futures on the S&P 500 nudged higher in after-hours trading.

But in a sign that investors were growing increasingly intolerant of the war’s continued impact on global energy prices, the selling began again on Friday morning, accelerating through the day to a 1.7 percent loss for the index.

Stocks in Europe and Asia were also broadly lower on Friday. The Japanese Nikkei 225 index ended the day 0.4 percent lower. The German Dax fell 1.4 percent, while the British FTSE 100 inched lower.

These short-term price swings are proving to be a headache for traders.

Markets have swung sharply each day as investors learn more about the conflict, moving higher on signs of de-escalation, and lower after attacks on important energy infrastructure. But this news-driven noise has tended to result in fairly muted moves by the end of each trading day. The index has fallen an average of just 0.3 percent per day since the war began through Thursday, but it has swung by an average of more than 1.3 percent between its high and low each day.

“For trading desks, it has been a really unpleasant time,” said Stuart Kaiser, an equity strategist at Citigroup. “It’s death by a thousand cuts.”

And there are signs that the market may be at a tipping point, say analysts and investors.

The tech-heavy Nasdaq Composite index fell into correction on Thursday, defined as a sell-off of more than 10 percent from its recent high. The Russell 2000 index of smaller companies seen as more tied to the domestic economy fell into correction in the final minutes of trading Friday, as did the Dow Jones industrial average.

And the sell-off has been broad. Every sector of the S&P 500 is in the red since the war began on Feb. 28 except the energy sector, which includes oil companies that benefit from higher oil prices.

Companies tend to lock in the price they pay for energy well in advance so many are not feeling an immediate impact from the increase in oil prices, and investors have been able to initially shrug off it off.

But that changes the longer oil prices remain elevated. Brent crude, the international oil benchmark, has risen sharply since the war began, from $72.48 per barrel to more than $112. But its future prices had remained lower. That has started to shift, said Mr. Kaiser, with Brent now expected to remain above $80 per barrel through the middle of next year, up from $76 two weeks ago, and above $75 for another year after that.

“That has spooked investors a bit,” he said.

As higher-for-longer oil prices have started to be priced into the market, so has the likelihood of lingering inflation and persistently higher interest rates.

The 10-year Treasury yield, which reflects the government’s borrowing costs over a decade and underpins consumer and corporate borrowing worldwide, has risen sharply since the war began.

The 10-year yield has surged roughly half a percentage point, to 4.43 percent. It is on course for its biggest one-month move higher since 2022, when the Federal Reserve rapidly raised interest rates to combat intense inflation.

The 10-year yield underpins the U.S. mortgage market where rates have moved higher in tandem, with the average 30-year mortgage in the U.S. rising sharply this month to around 6.5 percent.

The Fed has said that the war’s inflationary impact would likely prevent it from lowering interest rates soon. Investors expect the central bank to pause cuts for at least the next year.

International markets have fared even worse. Asia is the main destination for much of the oil exports that are blocked by the war. Europe is also heavily dependent on oil from the region and its economy is being battered by the fluctuations in global oil prices.

The Pan-European Stoxx 600 index has dropped nearly 10 percent since the war began, while bourses in London, Germany, France and Italy have all fallen into correction. The yield on 10-year government Gilts in Britain has risen by over 0.7 percentage points, while German Bunds have climbed roughly 0.4 percentage points.

A sharp move higher in the value of the dollar has compounded international worries, by making the cost of purchasing oil — which is largely traded in dollars — even higher.

The question that investors around the world are asking is, just how long will this last? The administration has been sending mixed signals on the future course of the conflict, proposing peace plans while sending soldiers to the region. On Friday, Iran turned back three container ships from crossing the Strait of Hormuz.

“It’s the challenge of our sitting president,” said Ms. Beaulieu. She added,

“It’s very difficult to predict where markets will end up or where the economy is headed right now.”

Joe Rennison writes about financial markets, a beat that ranges from chronicling the vagaries of the stock market to explaining the often-inscrutable trading decisions of Wall Street insiders.

The post Stocks Slide to 5th Weekly Loss as Investors Lose Patience With Iran War appeared first on New York Times.