Financial fear is a universal language right now.

These days, I often get stopped in the supermarket aisles, after a workout or at church. From young adults to retirees, the faces change, but the questions remain the same.

People are wondering if they should prepare for a market crash as the conflict with Iran worsens. Anxious savers question whether it’s time to withdraw their money from the bank and keep it at home. Families are concerned about whether Social Security will still be there for them or whether the Trump administration will drastically alter the benefits they have spent a lifetime earning.

These aren’t simply nervous ramblings. They are the logical reactions of folks watching the price at the pump rise while the Strait of Hormuz remains largely impassable.

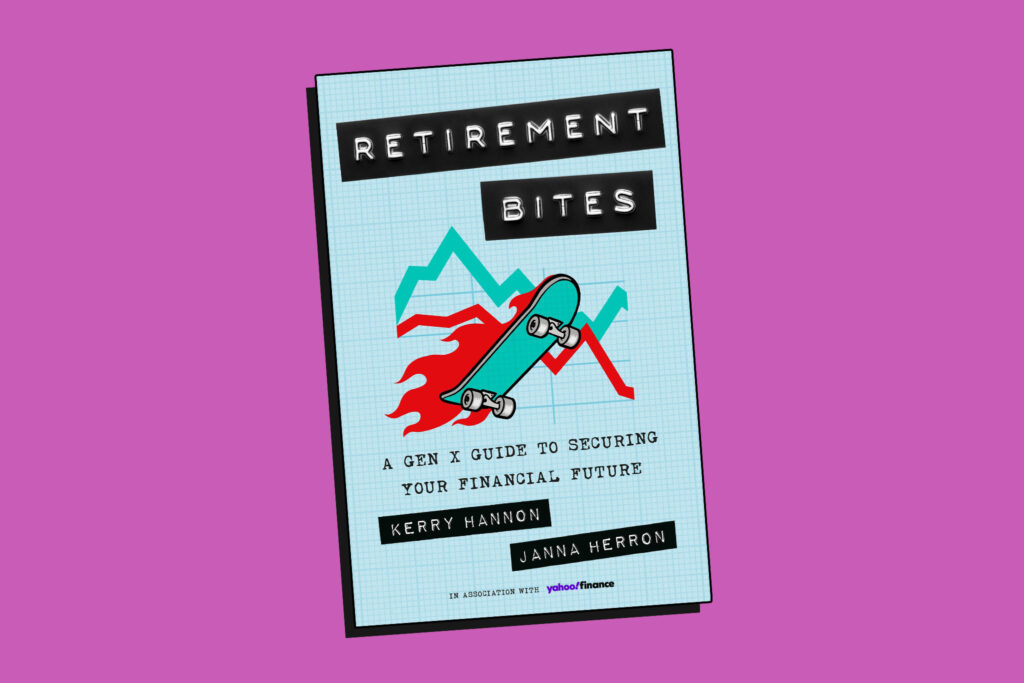

It’s precisely this climate of uncertainty that makes this month’s Color of Money Book Club pick so relevant. I’ve chosen “Retirement Bites: A Gen X Guide to Securing Your Financial Future” by Kerry Hannon and Janna Herron, both seasoned personal finance writers.

The title is a wink at “Reality Bites,” the 1994 film that defined Gen X’s early struggle to find its footing in the adult world. They are now facing the angst of retirement.

Gen Xers (the youngest turning 46 this year, the oldest 61) are a financially strained group. With pensions disappearing, persistent inflation concerns, rising health care costs, lingering student loan debt and a war of choice hitting the stock market hard, they are justified in worrying about retirement security.

Here are some sobering numbers about this generation, according to the authors’ research:

— A quarter of Gen Xers don’t have a retirement account. “When looking at median retirement savings levels for Generation X, the bottom half of earners have only a few thousand dollars saved for retirement, and the typical household has only $40,000 in retirement savings,” according to a 2023 report from the National Institute on Retirement Security.

— The majority of the 64 million born between 1965 and 1980 expect to postpone their retirement.

— They carry the most in average credit card debt ($9,600 in 2025, according to Experian). And they had the highest average student loan balance, owing $44,240 in 2024, according to a report by the Education Data Initiative.

— Two-thirds are living paycheck to paycheck.

— More than 7 in 10 Americans between the ages of 35 and 60 are caregivers for both their children and parents.

If you’re part of this “sandwich generation,” the pressures of elder and child care costs, along with an unpredictable global economy, can cause depression or stress about your financial situation.

“But we’re here to say it’s not time to give up,” the authors write.

Feel what you must, but then it’s important that you manage what you can, they encourage.

“Our ultimate goal is to get you where you can visualize a comfortable retirement — even as new challenges may arise — but not be overwhelmed by the steps you need to take to get there.”

You can’t control global oil prices or geopolitical tensions, but you can control your response to them. One way to handle financial uncertainty is to arm yourself with information. This isn’t leisure reading, but it’s a blueprint for a road out of the economic anxiety.

Hannon and Herron don’t start with spreadsheets; they start with your head. It’s a necessary beginning, because your attitude can stall even the best-laid plans.

This journey begins with this question: What’s your financial backstory?

Think back to your childhood. Did you grow up in a household where fights about money were so common that now you avoid conversations about it at all costs? Were you so overindulged as a child that you connect your self-worth to the stuff you own?

The authors encourage you to journal about how your memories of money affect your financial habits.

I have long believed in exploring the connection between your history and your financial habits or the emotional triggers that can prevent better money management.

If you grew up in a household where money was a source of trauma, you might find yourself as an adult either obsessively hoarding cash out of fear or impulsively spending to compensate for past deprivation. You can’t maintain the discipline needed for a 20- or 30-year retirement plan if you haven’t identified the money scripts you inherited.

Looking back, you can gain the clarity to distinguish between needs and wants, a skill that becomes vital when you eventually switch to living on a fixed income.

Hannon and Herron recognize that you can’t build a stable retirement on a fragile emotional foundation. Before examining the numbers, you must look in the mirror and admit that the child you once were often makes the adult’s financial choices.

Once the emotional ground is cleared, the authors pivot to the traditional terrain of personal finance. They cover a wide range of topics, from creating a net worth statement to understanding your 401(k), the realities of working longer, optimizing Social Security, and navigating the maze of Medicare and health care costs, all while balancing myriad other financial priorities.

Hannon and Herron don’t promise a miracle financial fix, but they offer practical advice to the biting reality of our current economy without having to cover your eyes.

As for the book club, we don’t meet in person. But I would love to know what you think of my picks. Email your comments to [email protected]. In the subject line put “Color of Money Book Club.” I’ll feature the feedback in my weekly newsletter. You can subscribe (it’s free) here.

–

The post Gen Xers are facing a new era of economic instability appeared first on Washington Post.